Posted: February 18, 2026 | Updated: February 19, 2026 at 9:18 AM

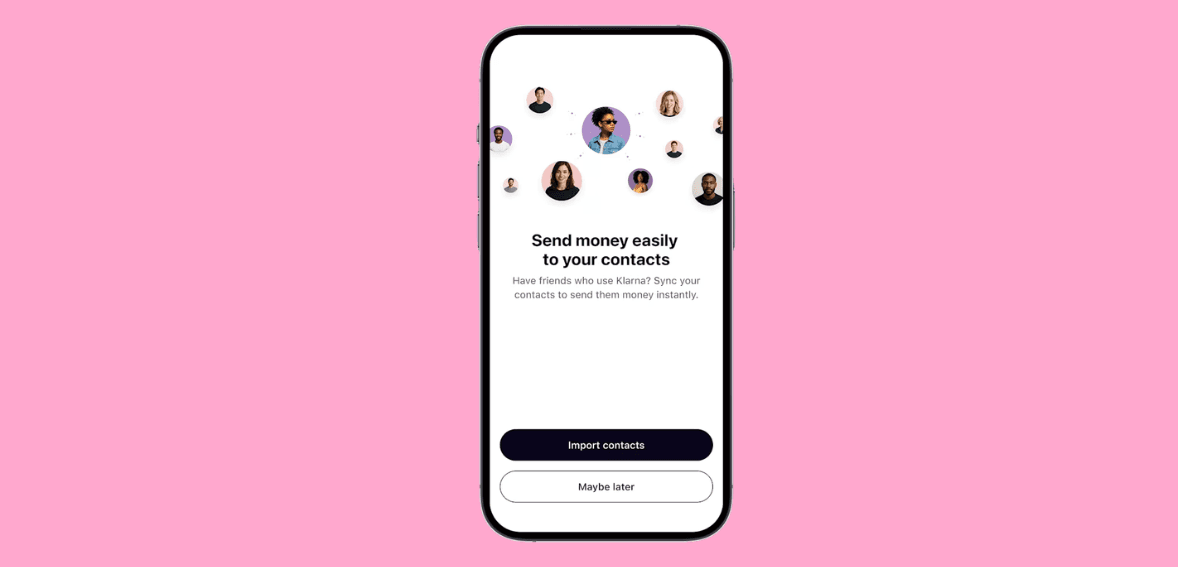

Klarna peer-to-peer payment feature is now available on the Klarna app. This feature allows users in 13 European countries to send money to friends and family using a phone number, email, saved contact, or QR code. Users can split bills or send money securely, as Klarna performs fraud and eligibility checks before completing each transfer.

The service has been introduced in countries including Belgium, Denmark, Finland, France, and Germany, and is currently available only for transactions between Klarna users. The company plans to expand the feature to non-Klarna customers and enable cross-border transfers in the future.

On January 14, 2026, Klarna launched an instant peer-to-peer payments feature on the Klarna app that lets users send money to their friends and family. This “cash-like” feature is backed by regulated banks. The feature was launched across 13 European markets:

Users can handle everyday transfers like splitting bills, paying back friends, sending money to their family, etc., instantly without leaving the application. The transfer process is simple:

Klarna is positioning this feature as a step towards everyday banking and money management, striving to move beyond its “buy now, pay later” identity.

Ever since Klarna Balance launched in 2024, global deposits have been on a steady rise. The company recorded $9.5 billion during the launch to $14 billion by September 2025. In October 2025, Klarna received e-money authorization and introduced a digital wallet and debit card in the UK. During the launch, the company said that authorization was a crucial aspect that would help them “disrupt” retail banking so Klarna can be the preferred choice for UK customers. After a few months of launch, the company recorded over 4 million sign-ups. These metrics show that users are shifting more daily transactions onto Klarna and creating a “flywheel” where higher engagement supports the adoption of additional banking features like P2P.

Klarna CEO Sebastian Siemiatkowski said customers are frustrated by friction in payment transactions and high traditional banking fees, prompting customers to look for a simpler and cheaper payment experience. Adding P2P turns Klarna from a platform that helps users pay merchants into one that also helps users settle with each other.

It’s also a good addition in the lineup of features like refunds and cashback flows into Balance accounts, since funds held in the app become more useful when they can be sent out instantly to other people rather than only spent at merchants or withdrawn.

Some experts are signaling caution as P2P systems are high-risk because these systems prioritize speed. This service is also similar to the one offered by Zelle, and they are recently facing criticism over scams and fraud because the transactions are instant and hard to reverse once money is debited from the account. As mentioned, the company has emphasized security during the launch, stating that it will conduct fraud and eligibility checks before allowing a transfer.

In the long term, Klarna is also experimenting with new rails and partnerships that broaden account-to-account payments. The current P2P system runs on banking rails, and Klarna highlighted that they are openly exploring other stablecoin-based options to enhance reach, speed, and efficiency.

And in November 2025, Klarna partnered with Sparkassen-Finanzgruppe to launch variable recurring payments (VRPs). It’s an open-banking method that lets customers authorize payments from their bank accounts within agreed limits and is an alternative to direct debits, which are useful for subscriptions, memberships, and other recurring charges.

Currently, it’s unclear whether the product will launch in the U.S. anytime soon. The company stated it intends to bring it to the U.S. but has no immediate plans for a U.S. launch. That may be because of the regulations and existing P2P platforms like Venmo or Zelle. Klarna is currently focusing on deploying quickly across multiple countries, where it already has established banking products, and using adoption data and risk learnings to guide any future rollout.

Klarna is a global digital bank and payments provider. Klarna is led by co-founder and CEO Sebastian Siemiatkowski, with Niclas Neglén as CFO. The company is best known for “buy now, pay later” alongside a growing set of everyday money tools for consumers and commerce tools for merchants. Founded in 2005 in Stockholm, Sweden, the company has grown from online checkout and short-term credit into a broader app experience that also includes accounts, a debit-first card, and person-to-person payments in select markets.

Till now, Klarna has served 114+ million active users and processed about 3.4 million transactions per day, and worked with 850,000+ retailers globally. It has operated under a banking license in Europe (granted by the Swedish Financial Supervisory Authority) and has expanded UK capabilities through authorization for its UK subsidiary as an Electronic Money Institution by the Financial Conduct Authority.

Klarna’s P2P payment feature is a new offering designed to reinforce its positioning as an application “useful beyond checkout.” Now users across 13 European markets can send money instantly to each other using phone number, email, saved contact, or QR code. With fraud and eligibility checks, users benefit from the reduced risks associated with real-time transfers.

While the feature is currently limited to transfers between Klarna users, the planned expansion to pay non-users and enable cross-border transfers would significantly increase its everyday utility and further shift Klarna’s position from a buy now, pay later brand to a broader digital-banking “hub” for spending, storing, and moving money.

Klarna’s P2P feature lets you send money to your friends and family directly from the Klarna app. It’s just like Venmo or Zelle. Users can make the transfer by scanning QR or selecting a contact using phone number or email. The money is debited from the sender’s Klarna account to the recipient’s Klarna account instantly. Currently, the feature works only if both parties have Klarna in one of the 13 regions where the feature was initially launched.

No. Klarna launched P2P payments in 13 European countries, which include Belgium, Denmark, Finland, France, Germany, Italy, the Netherlands, Norway, Poland, Portugal, Spain, Sweden, and the United Kingdom. The company’s spokesperson specifically said that they do not have immediate rollout plans for the U.S. yet. The U.S. market already has entrenched P2P options, plus regulatory requirements differ.

Klarna is well aware of the fraud risks surrounding P2P payments. That’s why they have built a fraud and eligibility check system to safeguard the transactions. While details are scant, this could mean Klarna might restrict new users from sending large amounts until verified, or use AI to flag suspicious patterns. Also, because Klarna holds banking licenses in Europe, there are regulations requiring things like customer identity verification (KYC) and transaction monitoring.

Functionality-wise, it’s similar. It’s instant and free to send money to others on the same platform. The main difference is that Klarna’s services are tied to having a Klarna account. It’s very much like Revolut’s transfer feature or N26’s MoneyBeam in Europe. Compared to PayPal, Klarna’s probably trying to make it more social and seamless within a shopping app. The main competitive edge Klarna has is its large user base from BNPL. Now they’ll see a “Send Money” option in the app, which could quickly gain traction.